Everything You Need to Know About PAN (Permanent Account Number)

In today’s world of finance and taxation, a Permanent Account Number (PAN) is not just an important identifier—it’s essential for anyone living in India who wants to manage their finances legally and effectively. Whether you’re an individual, a business, or a professional, PAN plays a crucial role in ensuring your transactions are smooth, your taxes are paid, and your identity in the financial system is secure.

This blog will take you through everything there is to know about PAN. We’ll discuss its full form, its importance, how you can get one, and the numerous benefits it offers. By the end of this guide, you’ll have a complete understanding of PAN and why you should have one.

What is PAN?

Permanent Account Number (PAN) is a 10-digit unique identifier issued by the Income Tax Department of India. It’s mainly used to track an individual’s or an entity’s financial transactions and helps in maintaining an organized record for taxation purposes. Every PAN number is unique and has no expiration date, making it “permanent.”

The PAN is essentially used to:

- Track the income and tax-related activities of individuals and entities

- Serve as an identification for filing income tax returns (ITR)

- Act as a tool for preventing tax evasion

- Streamline financial transactions for individuals and organizations

PAN Full Form

As mentioned earlier, PAN stands for Permanent Account Number. Let’s break it down:

- Permanent: The PAN remains the same throughout your life.

- Account: It is linked to your financial and tax records.

- Number: The identifier is numerical, comprising a combination of alphabets and numbers.

Unlike other identification numbers (like your Aadhaar or Voter ID), PAN is specifically linked to your financial transactions and acts as a crucial part of India’s tax infrastructure.

Why is PAN Important?

1. Essential for Tax Filing

The primary use of PAN is for filing income tax returns (ITR). Without it, you won’t be able to file your taxes, as the government relies on PAN to track your earnings and tax contributions. Whether you’re filing a personal return or for a business, PAN is required.

2. For Financial Transactions

A PAN is needed for many financial activities, such as:

- Opening a bank account

- Purchasing property

- Investing in stocks or bonds

- Receiving income above a certain limit

It serves as a proof of your identity for financial institutions, making your transactions more secure and traceable.

3. For Tax Deduction and Collection

When you earn income, a portion of it is often deducted at the source as tax. The Tax Deducted at Source (TDS) system uses PAN to ensure that tax payments are correctly credited. This helps in preventing double taxation and evasion.

4. Preventing Tax Evasion

PAN helps in maintaining transparency in financial dealings. By linking every transaction to a unique PAN, the Income Tax Department can track who’s receiving payments and from where. This ensures that tax payments are properly made and prevents tax evasion.

5. For Business Transactions

For businesses, having a PAN is mandatory for:

- Filing business taxes (including GST and income tax returns)

- Conducting large financial transactions

- Opening a business bank account

Thus, PAN is equally important for companies and businesses as it is for individuals.

Who Needs PAN?

Now that we know how vital PAN is, you might be wondering, “Who exactly needs it?”

In India, PAN is mandatory for:

- Indian Citizens: Anyone earning above a certain income threshold, or involved in significant financial transactions, needs to have PAN.

- Non-Resident Indians (NRIs): PAN is also required for NRIs who want to invest in Indian stocks, file tax returns, or engage in other financial activities.

- Foreign Nationals: If you’re a foreign national living in India and involved in financial or investment transactions, you may also need a PAN.

- Businesses and Companies: PAN is essential for all types of businesses, including private limited companies, public limited companies, LLPs, and partnerships, who need to conduct financial transactions or file returns.

How to Apply for PAN?

Applying for PAN has become a very simple and streamlined process. Here’s how you can go about it:

Step 1: Choose the Correct Application Form

You can apply for PAN through the official NSDL or UTIITSL websites. The form required for individuals is Form 49A, and for foreign nationals, Form 49AA is used.

Step 2: Fill in the Application Form

The form requires your basic details, such as:

- Name

- Father’s name

- Date of birth

- Address

- Contact details

Step 3: Submit Identity Proof and Address Proof

You’ll need to upload or provide documents that prove your identity and address. Some commonly accepted documents include:

- Aadhaar card

- Voter ID

- Passport

- Utility bills (for address proof)

Step 4: Payment of Fees

PAN application comes with a nominal fee. Payment can be made online via debit/credit card, net banking, or demand draft.

Step 5: Receive PAN

Once the application is submitted, the Income Tax Department processes it. You’ll receive your e-PAN within a few days, which is an electronically generated version of your PAN card. The physical PAN card will be sent to your registered address.

What is an e-PAN?

In addition to the physical PAN card, the Income Tax Department has introduced the e-PAN. It is an electronic version of your PAN card, which can be downloaded from the official portal. The e-PAN is equally valid as the physical PAN card and is widely accepted for various financial and tax-related purposes.

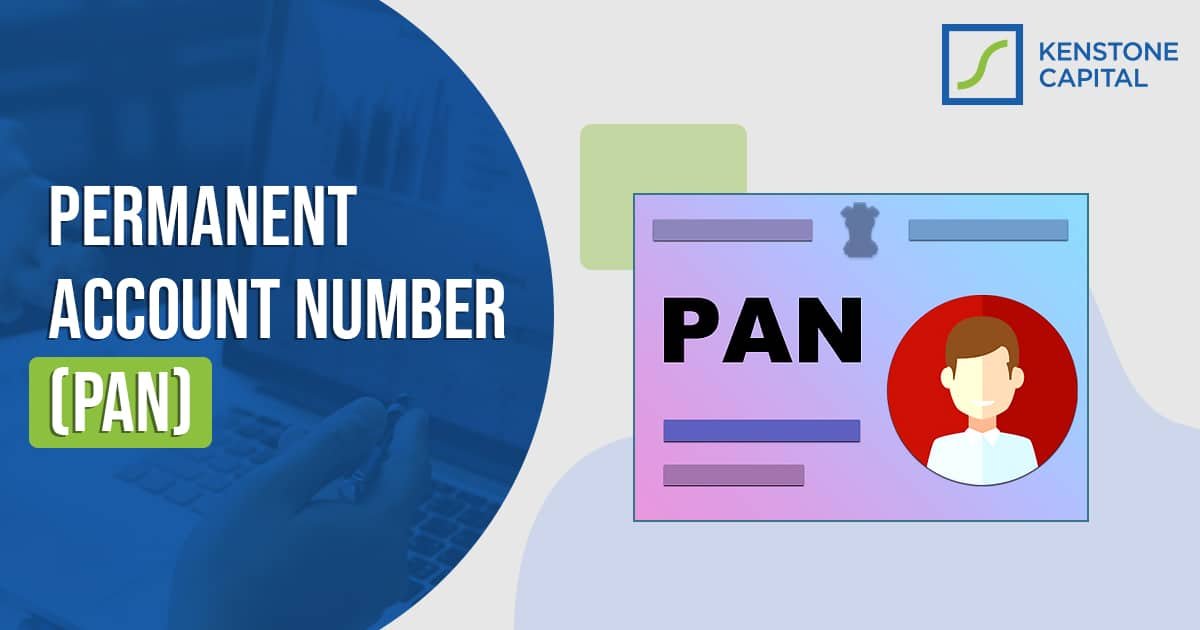

PAN Card Format

A PAN card consists of 10 characters:

- The first five characters are letters.

- The next four characters are numbers.

- The last character is a letter.

Here’s an example format of a PAN number: ABCDE1234F

- The first three letters are random alphabets.

- The fourth character is a letter denoting the type of entity (e.g., “P” for individuals, “C” for companies).

- The fifth character is another random letter.

- The next four digits are a unique numerical code.

- The last letter is a check code.

This unique combination helps ensure that each PAN number is distinct and can be used to identify the person or entity in the financial system.

Benefits of PAN

1. Tax Efficiency

PAN helps in ensuring that taxes are paid on time and in the correct amount. It allows for better tracking of tax payments, reducing the chances of errors or discrepancies in tax calculations.

2. Simplicity in Financial Transactions

Having a PAN allows you to conduct major financial transactions, such as buying a house or car, without facing any legal hurdles. Financial institutions and banks need PAN details for smooth processing.

3. Easy to Track Your Income

Since PAN tracks all financial transactions, it becomes easier for individuals to manage their finances. You can view all your earnings and tax payments in a single record, helping you stay organized.

4. Helps in Taking Loans

PAN is mandatory when applying for loans, whether it’s a personal loan, car loan, or home loan. Lenders require PAN to verify your creditworthiness and income sources.

Common Problems with PAN

Though PAN is an essential document, there are a few common issues people face regarding their PAN:

1. Lost or Damaged PAN Card

If you lose your PAN card, don’t panic. You can easily apply for a duplicate card through the official portal. All you need to do is submit an online request along with a fee.

2. Incorrect Details

Sometimes, the details on your PAN card may be incorrect, such as a misspelled name or a wrong date of birth. This can be rectified by applying for a correction in your PAN card details.

3. Linking PAN with Aadhaar

With the government’s push towards digitalization, it’s mandatory to link your PAN with Aadhaar. This can be done online through the Income Tax portal, making your financial records more secure.

Conclusion

In the fast-paced world of finance and taxation, having a Permanent Account Number (PAN) is more than just a necessity. It’s a gateway to smooth financial transactions, tax filing, and a transparent financial system. Whether you’re an individual, business, or professional, PAN ensures that your transactions are traceable, secure, and legitimate.

If you haven’t applied for your PAN yet, now is the time to do so! It’s quick, easy, and an essential tool for managing your financial life in India.

What are your thoughts about PAN? Is there something you’ve learned today about PAN that you didn’t know before? Feel free to share your experience or ask questions in the comments below!